People need to sustain their retirement planning work while making smart financial choices throughout their entire life. People tend to commit tiny errors which result in significant consequences during their later life stages. People make these mistakes because they do not detect them until their retirement period begins. People need to learn about the most common mistakes which lead to financial problems so they can protect their future through better choices. The following list includes ten common financial errors which can harm your ability to save money for retirement.

Delaying Retirement Savings

People who make even tiny regular investments during the first years of their financial journey will see their wealth increase substantially after several decades. For example, someone who begins investing at 25 needs far less monthly contribution than someone starting at 40.

Underestimating Living Costs

People believe that their expenses will decrease after they retire yet their spending on essential goods such as groceries and utilities and their traveling expenses and their healthcare needs will maintain high levels. Some studies suggest retirees may need 70% of their pre-retirement income to maintain their lifestyle.

Relying Only on One Income Source

People who depend solely on their pension benefits and government assistance programs like Social Security face financial danger. People who create multiple revenue streams through their savings and investments and rental properties will achieve stronger financial protection.

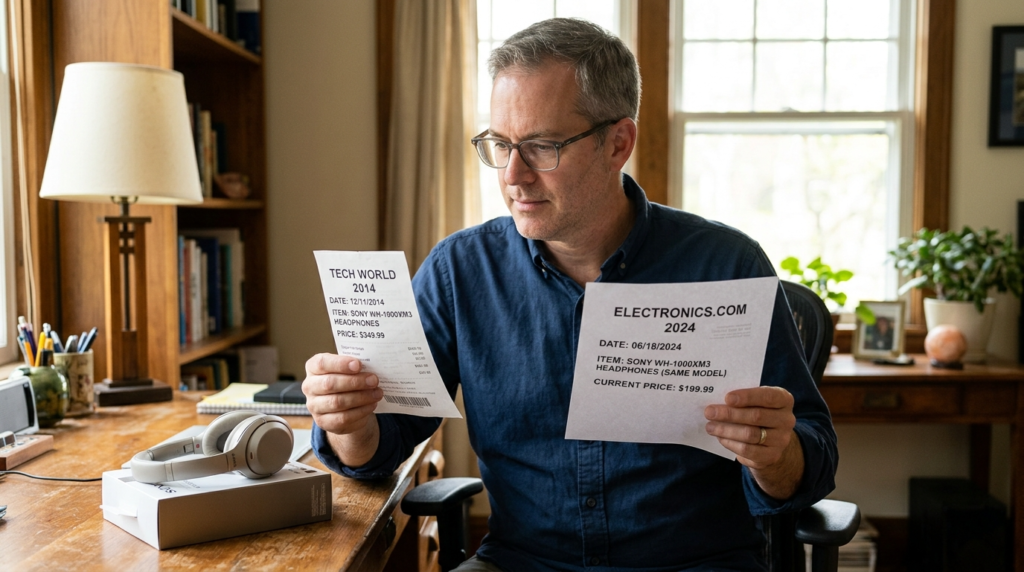

Ignoring Inflation

It would not be wrong to say that inflation steadily decreases the actual value of money. Your expenses will double after 20 to 25 years when your inflation rate stays at 3 percent. Your savings will run out because you did not account for this situation.

Withdrawing Savings Too Early

You lose both your original amount and your investment earnings when you take out money too soon. People use the “4 percent rule” to create spending limits which protect them from running out of money but withdrawing more can increase the risk of depleting funds.

Not Managing Debt Before Retirement

Earning fixed retirement income becomes difficult when people maintain debt obligations that include high-interest credit card debt. The financial burden on people decreases when they complete their loan obligations before reaching retirement age.

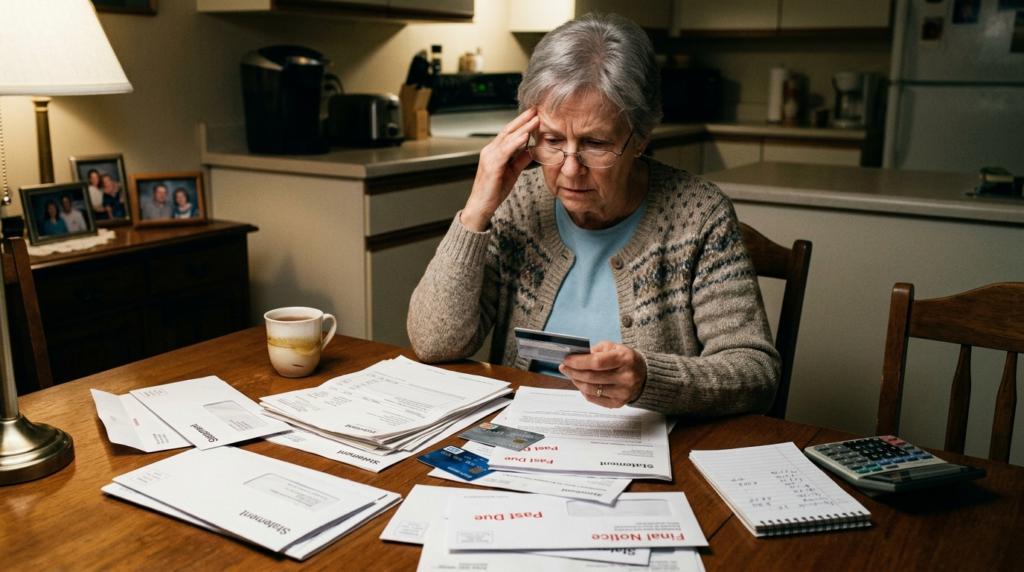

Lack of Emergency Fund

Unexpected expenses occur when people face medical emergencies or need home repairs or family support. Retirees who lack a dedicated emergency fund must rely on their long-term investments for urgent expenses.

Overlooking Healthcare Costs

Healthcare expenses represent the largest financial burden that retirees face. In the U.S., estimates suggest a retired couple may need $300,000+ over time for medical costs. People need to plan their insurance costs together with their out-of-pocket expenses.

Poor Investment Strategy

Investors who choose conservative strategies will experience inflation losses while aggressive investors risk losing their entire investments. All investors need to establish a balanced portfolio that changes according to their age through a process known as asset allocation.

Not Reviewing Financial Plans Regularly

Life changes occur through various factors which include changes in income and expenses and health conditions and market developments. The annual review of your financial plan enables you to track your progress while implementing required modifications.