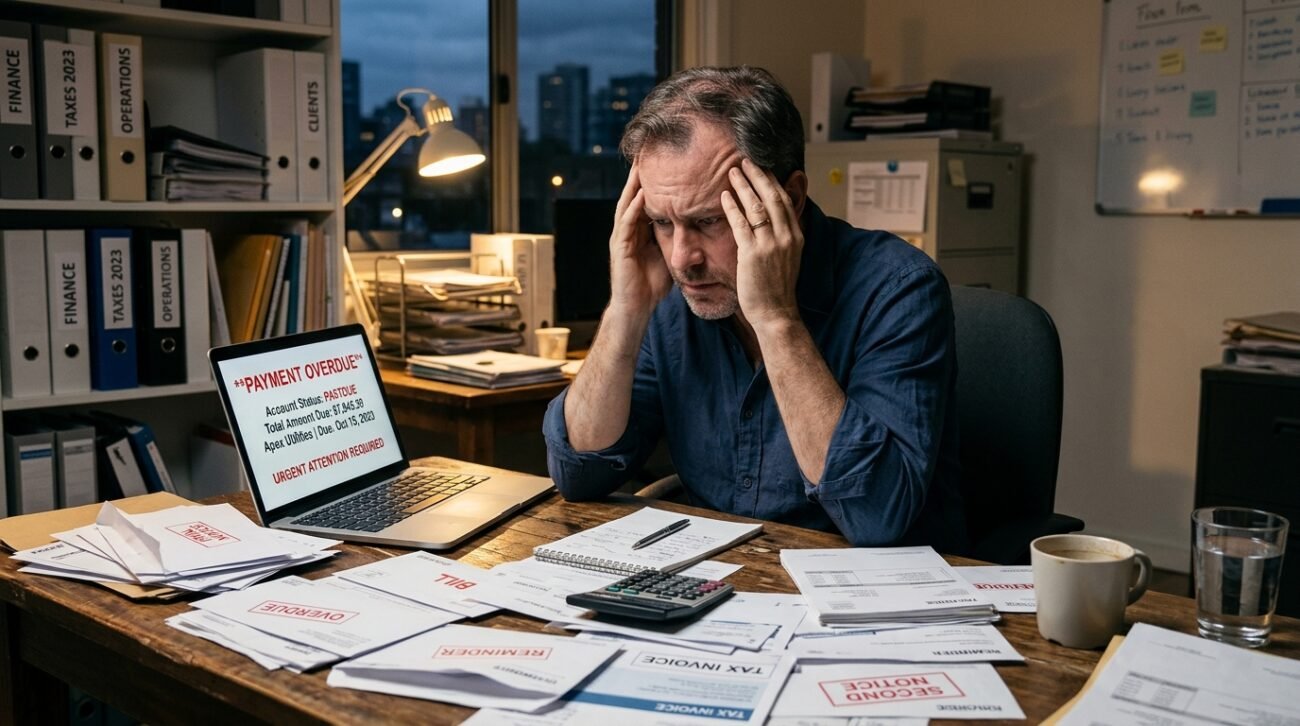

Missing a business loan payment can feel like a small slip but it can quickly escalate if not handled properly. Lenders treat missed payments seriously because they signal potential risk. The consequences depend on how late the payment is, the loan terms, and how you respond. You can reduce damage by learning the exact procedure which will help you take preventive measures.

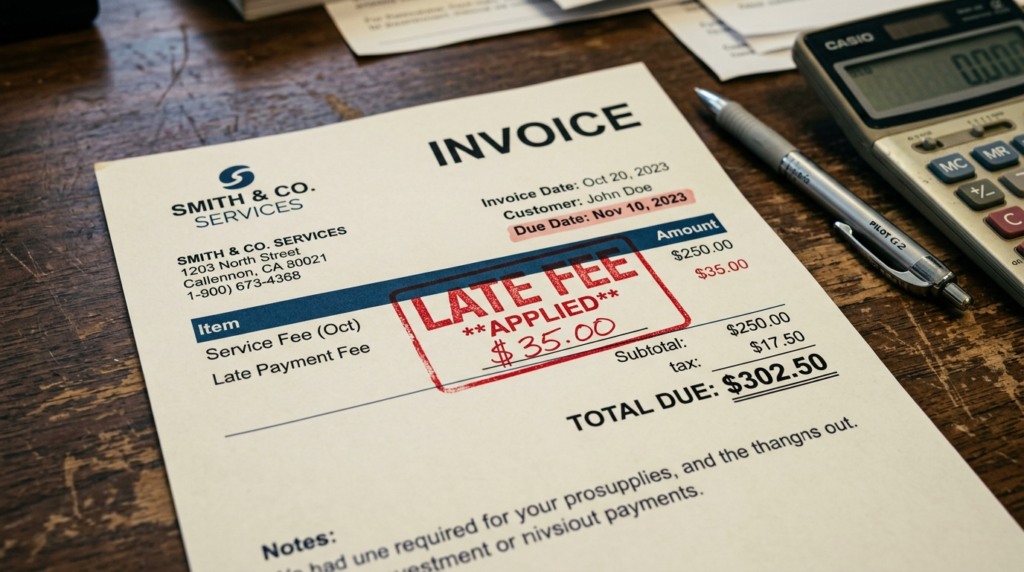

Late Fees Are Applied Almost Immediately

Most lenders impose a late fee when you fail to make a payment on time or after a brief grace period ends. These fees can range from 1–5% of the missed payment, which results in higher overall costs for you.

Your Credit Score Takes a Hit

Credit bureaus receive reports about your delay after it reaches 30 days. This situation can cause a major drop in your business or personal credit score which will make borrowing money in the future much harder.

Interest Continues to Accumulate

The outstanding balance keeps increasing because interest keeps accumulating after you miss your payment. The total amount you owe will increase through time as the outstanding balance grows.

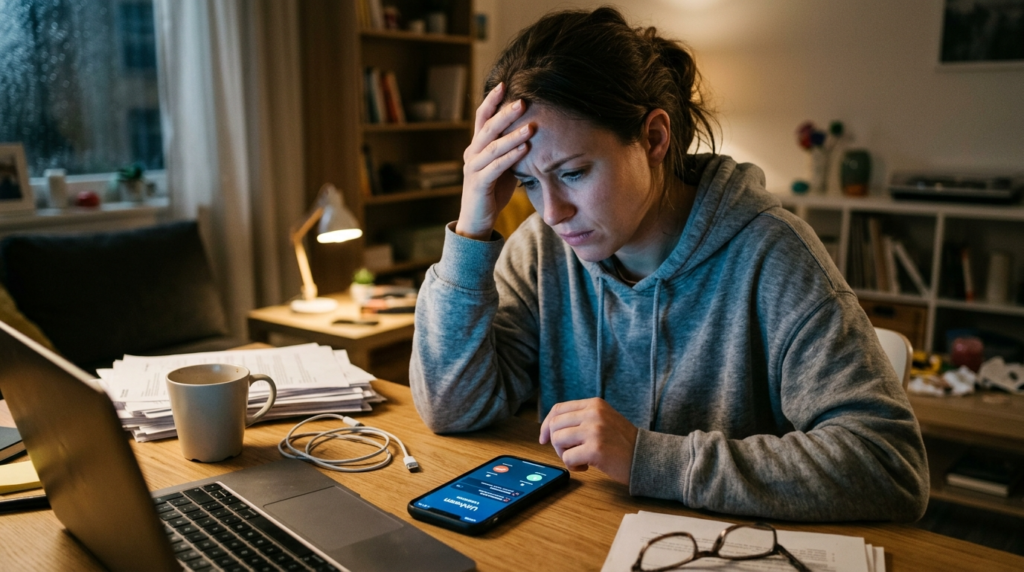

You Start Receiving Collection Calls

Lenders or recovery teams will start contacting you through phone calls and emails and text messages. Their objective is to retrieve overdue payments from you before the situation becomes worse.

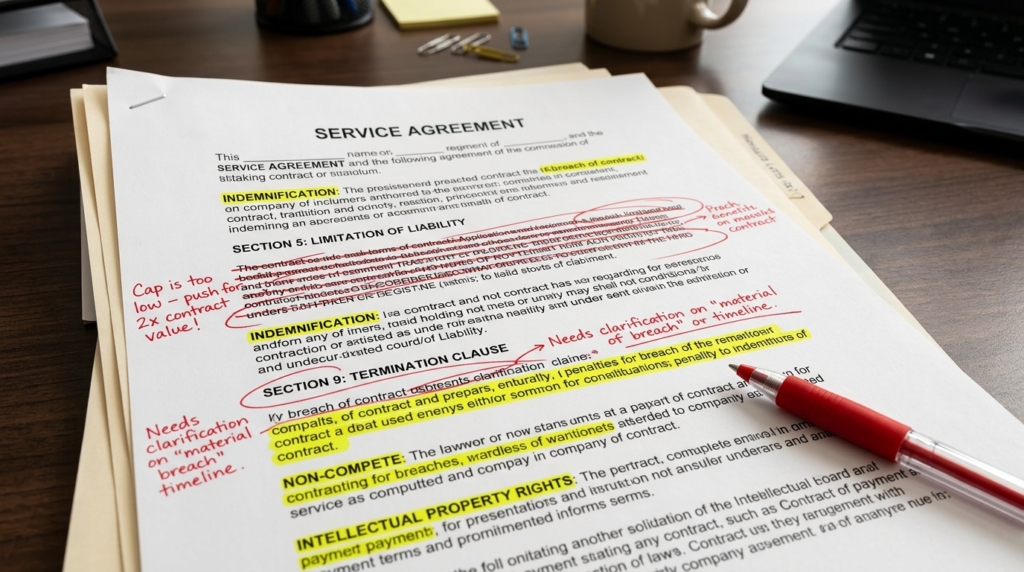

Loan Terms May Become Stricter

Some loan agreements include penalty clauses. Missing payments will result in higher interest rates and extra penalties together with more strict repayment requirements.

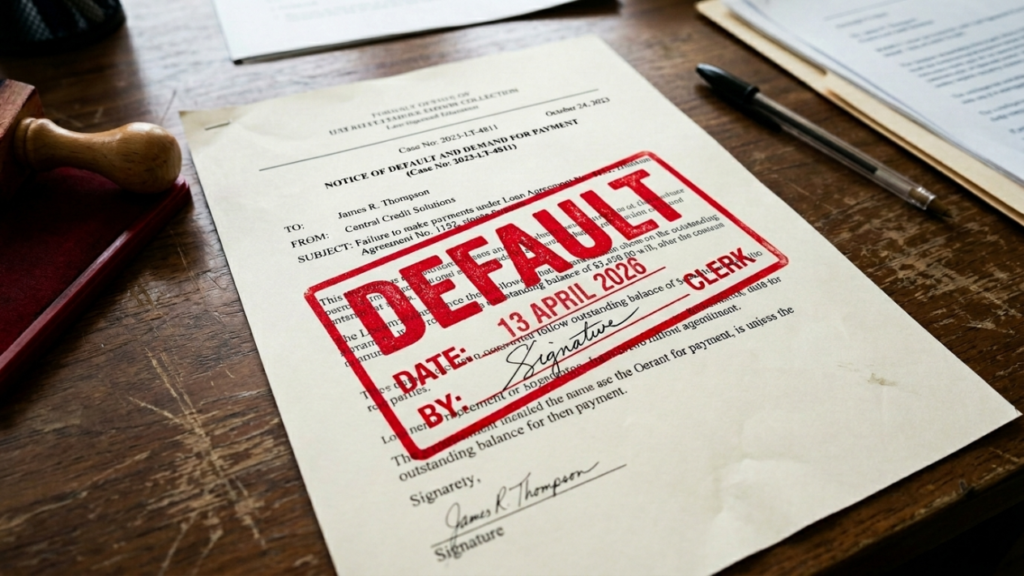

Risk of Loan Being Classified as Default

If payments are missed for an extended period (typically 90 days or more), the loan may be officially classified as a default or non-performing asset (NPA).

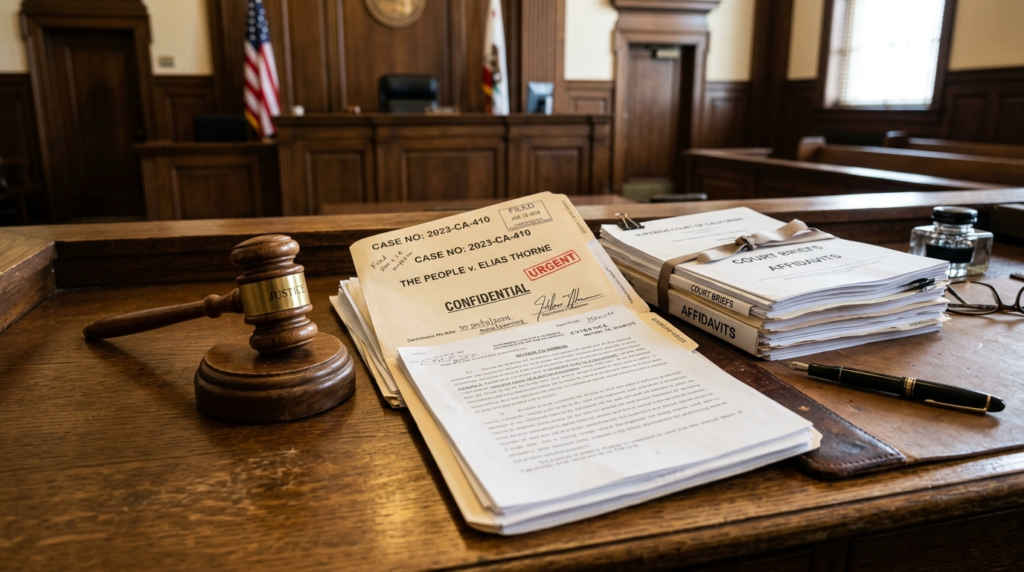

Legal Action Can Begin

Lenders may start legal proceedings to reclaim the loan in serious situations. The process includes court notifications together with legal procedures for recovering debts.

Assets or Collateral May Be Seized

Indeed, the lender can take control of the secured assets which the borrower has pledged as collateral when the loan is backed by security. Paying liabilities in time is a good way to save your assets or collateral intact.

Difficulty Accessing Future Credit

A history of defaulting on payments creates obstacles for obtaining various types of loans and credit lines while also restricting access to better interest rates. Lenders see you as high risk.

Stress on Business Operations

The business will experience operational difficulties because cash flow problems and debt repayment requirements will disrupt both daily activities and employee compensation and business expansion efforts.