Credit cards are being sold as easy, very flexible and rewarding and this is really the case with most of the people. Behind the flashy sign-up bonuses and cashback offers, however, the large credit card issuers have constructed a system capable of complicating the act of escaping debt and predicting the cost of interest. The end result is that millions of cardholders end up paying significantly higher fees and interest than they first projected without even understanding how policy structures are made to work against their favor. Financial gurus ensure that some of the usual habits and practices in the industry can lure even the disciplined user into costly cycles unless he or she is being keen. Knowing how to get your money to stay in your pocket and not the balance in credit card companies is maybe better now.

Large Interest Rates Which become activated within a short time

Most cards impose extremely high annual percentage rates (APR) which start charging interest immediately when you have a balance on your card, even a small one. Minimum amounts paid will make interest multiply quickly and prolong the time of repayment.

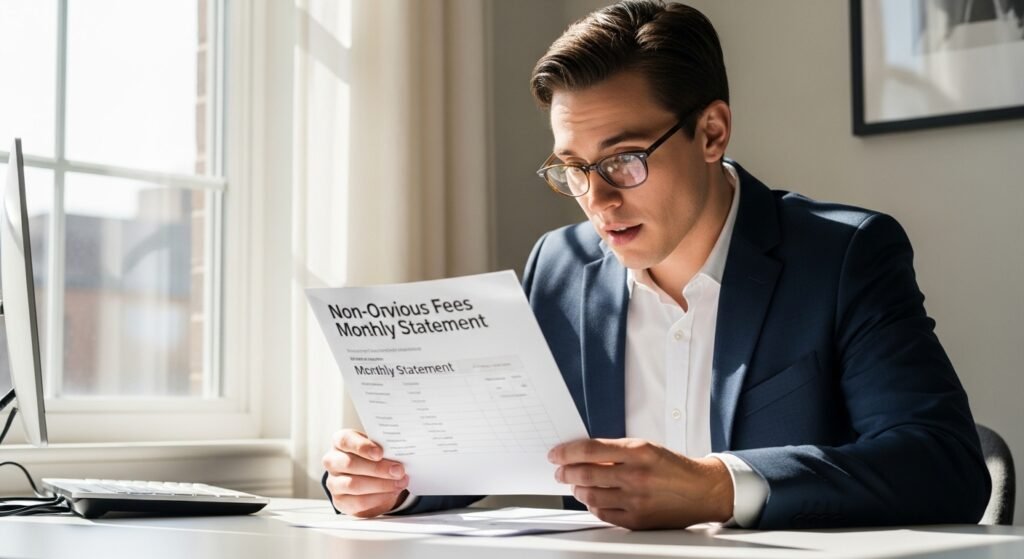

Non-Obvious Fees that the majority of users disregard

Over limit, late payment, balance transfer charges and foreign transactions cost can be accumulated within a short time. There are certain charges that would not be readily noticeable until they are reflected on your bill.

Reduced Minimum Payments Costing You More

Minimal payments imposed by credit card companies are very low by nature, just sufficient to pay interest. By just paying the minimum amount, you would extend your debt to a long period and pay a lot of interest in the long run.

The Rewards That Do Not Always Pay

Sign-up bonuses and rewards are luring, but reward models usually have a high expenditure prerequisite or yearly expenses that exceed their worth to most users.

The Tricks of balance transfer may backfire

Promotional balance transfer offers of 0% interest, which are offered on cards, might appear to be the best but transfer fee and fluctuation of rates after the promo period can make you lose more money when you fail to pay the amount before the stipulated time.

A Credit Score Can Be a Weapon

Carrying more than one card may enhance the use, yet it may also push you to unwanted expenditures. Late payments, large balances, and multiple credit checks would damage your credit in the long-term.

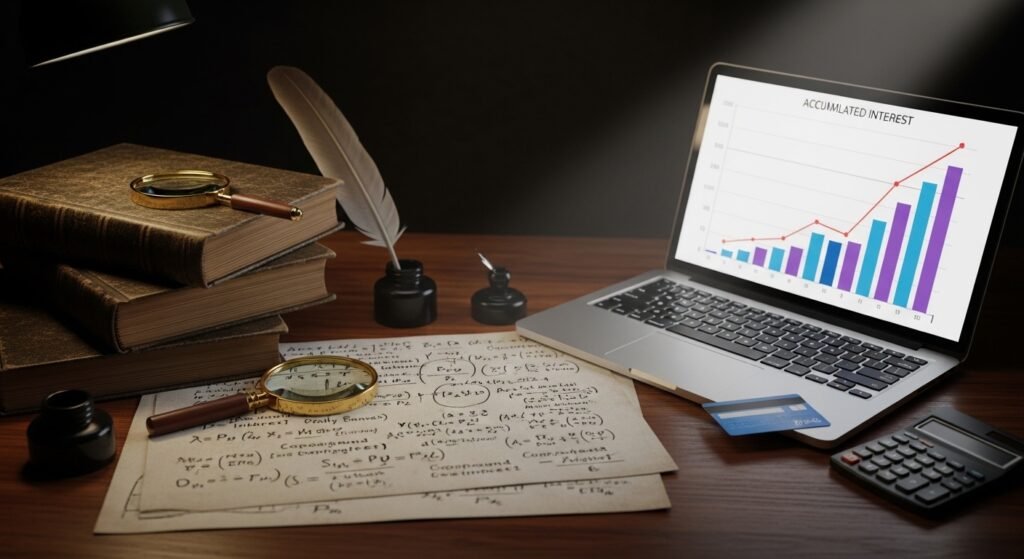

Use of Interest Calculation Mechanisms is Injurious to You

Such formulas of average daily balance or compound interest that banks tend to adopt ensure that interest accumulated is higher than you imagine – even when you consider yourself to be paying reasonably.

Automatic Renewals and Annual Fees

There are cards that automatically renew and charge annual fee automatically that you might not even recall signing up. These charges end up costing money annually without being reviewed.

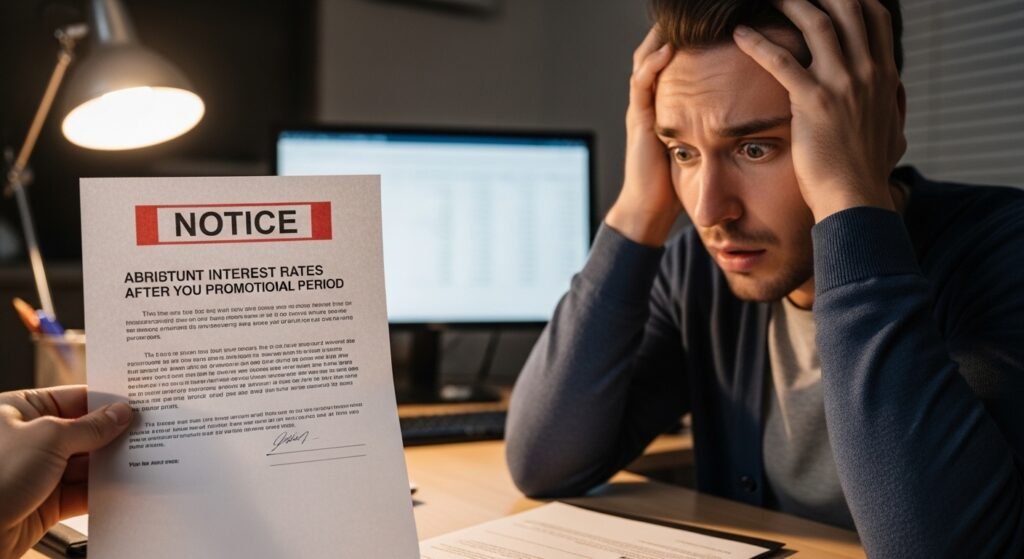

False Security Could Be generated by Intro Offers

APRs or teaser rates frequently are extinguished within a few months. Once the promotional period is over, the users that get accustomed to low rates may be struck with high interest at alarming notice.

Vicious Payment Distribution Policies

When you have a combination of balances you end up with making payments to the lower rate balances first off by the credit card issuers – which leaves the debt that is more costly hanging around longer.

Consciousness Is Your Best Security

The nucleus is that once you know how these systems work you will be in control. The easiest tips such as paying the full amount at the end of the month, examining the statements more closely and the right card according to your lifestyle can save you the debt traps and keep your finances in a healthy state.