People believe retiring at 62 enables them to enjoy their active life until their health starts to decline. Early retirement which means leaving work five years before most people reach their full retirement age requires you to honestly evaluate your financial situation and your current way of life. The assessment of your readiness requires you to assess your future financial needs beyond your current bank account balance against 30 years of expected retirement expenses.

Can You Bridge the Healthcare Gap?

Medicare starts on your 65th birthday as the date of its beginning. The 62-year-old retirees need to create a three-year plan which outlines their private health insurance expenditures. Couples should expect their monthly expenses to exceed 1000 dollars since medical costs tend to exceed their expectations. The person who does not possess an efficient method to deal with this coverage gap until they become 65 years old will deplete their savings after facing one medical emergency.

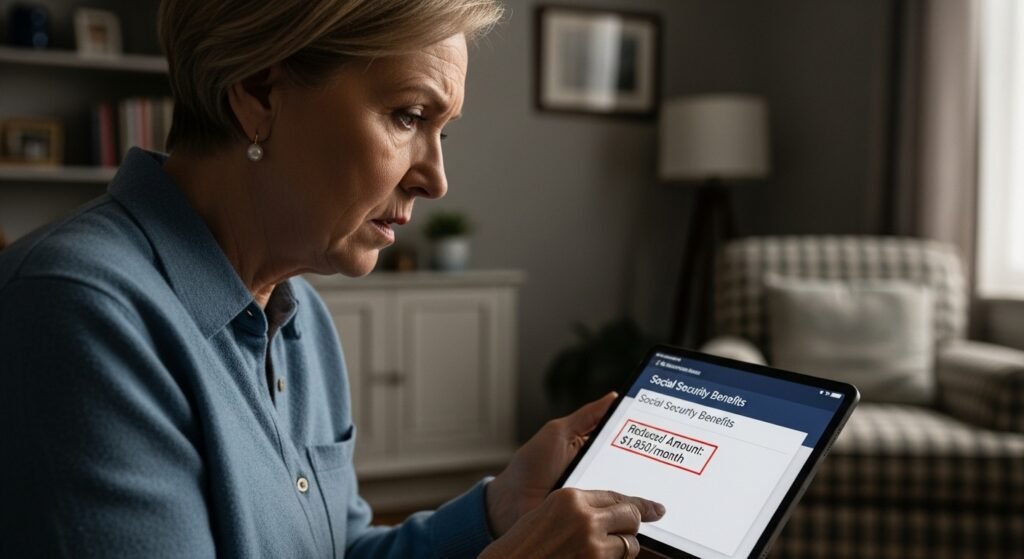

Have You Calculated the Social Security “Hit”?

Your Social Security payments will reduce by 30 percent if you choose 62 as your earliest retirement age. You need to ask yourself: Can I live comfortably on a much smaller check for the rest of my life, or do I need the full amount to cover my bills?

What is Your “Burn Rate”?

Do you understand your monthly living expenses? People generally spend less money than their actual expenses. You need to determine your retirement spending plan by calculating all your monthly expenses which include your housing costs and food expenses and utility bills and entertainment spending. Your savings will manage the deficit that occurs when your guaranteed income sources fail to fulfill your financial requirements.

Is Your Debt Truly Gone?

People who want to retire should eliminate all their home debt and vehicle debt and credit card debt to minimize their financial dangers. People who receive fixed payments from their investments face ongoing expenses since their interest payments result in continuous financial loss. The majority of successful early retirees aim to have their primary home paid off by age 62 to keep their monthly overhead as low as possible.

Do You Have an “Emergency Bucket”?

Market downturns happen. The stock market crash that occurs after your 62nd birthday makes it essential to sell your investments for dinner expenses, which will prevent you from reaching financial balance. The safe savings account should hold enough cash to support your expenses for 1 to 2 years during periods of market decline.

What is Your Plan for “Longevity Risk”?

People worry about running out of money during their retirement period. Most people in modern society will reach their 90th birthday because of advancements in medical science. You need to calculate if your savings can survive a 30-year withdrawal period without hitting zero.

Are You Emotionally Ready?

Retirement involves both financial matters and the distribution of time throughout your life. At 62, you are still young. You need to determine what activities you will do with 40-plus additional hours of time during each week of your life. Many early retirees experience boredom or identity loss after they stop their work because they lack a hobby or volunteer activity or second career.

Have You Factorized “Lumpy” Expenses?

Your monthly budget might look good, but what about the “lumpy” costs? You will need to replace your car and your roof and your dental care every few years. Your retirement plan must include a fund for these inevitable, large-scale expenses.

Can You Pass the “Trial Run”?

The best way to see if you can retire at 62 is to live on your projected retirement budget for six months while you are still working. The situation appears to create excessive pressure, therefore you need to work additional years until you acquire sufficient savings.