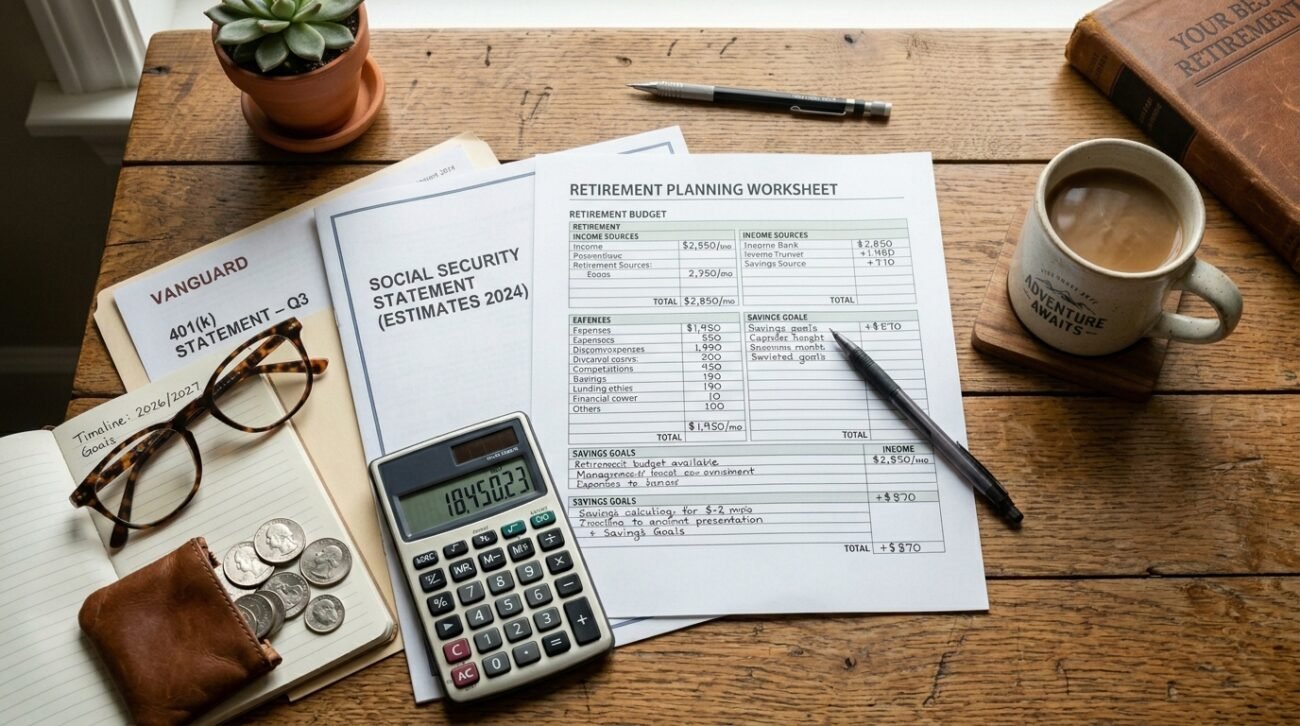

Retirement at 65 marks the transition from wage earning to responsible financial resource management. Creating a precise monthly budget serves as the vital requirement which enables people to achieve their desired level of financial security and emotional tranquility. Most retirees create budgets which follow standard patterns that include expenses for housing and healthcare and their regular daily needs. The complete analysis demonstrates a practical monthly budget which presents both the financial distribution and the retirement spending habits of individuals.

Housing Costs

Many retirees decrease their housing expenses by moving to smaller homes or smaller towns or by completing their mortgage payments before they retire. Financial stability requires people to manage their housing costs effectively.

Groceries and Food

Food expenses depend on personal dietary practices. People who prepare meals at home and purchase products in bulk while preventing food waste will achieve substantial savings. Retirees often maintain this balance through social dining experiences which they enjoy.

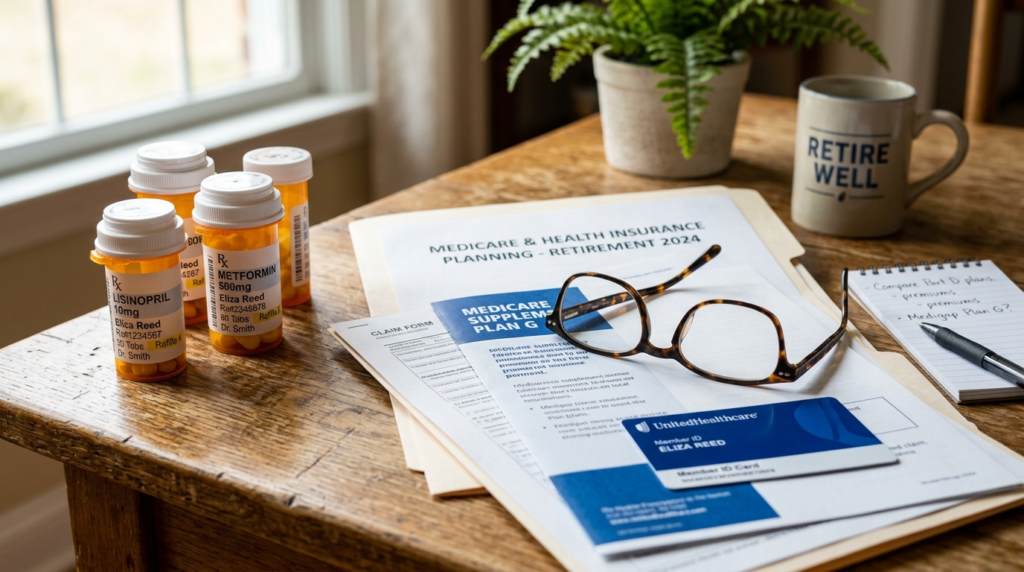

Healthcare and Insurance

This category represents one of the most essential sections. The total includes all costs associated with insurance and medications and doctor appointments and preventive health services. The costs associated with this category require people to maintain an expense buffer because costs will probably rise as they age.

Utilities

This category includes all monthly expenses for electricity and water and gas and internet and mobile phone services. Retirees control their expenses through usage reduction and selection of basic service packages and implementation of energy-saving devices.

Transportation

People need to pay for gas and public transportation and occasional taxi services. The elimination of commuting leads to reduced expenses which become lower than what people experienced during their employment period. Some retirees even give up owning a car to save more.

Personal and Household Expenses

People need basic items that include toiletries and cleaning products and clothing and small items that they use in their homes. The individual expenses which seem small begin to accumulate when they are combined.

Entertainment and Leisure

Retirement provides people with free time to pursue their hobbies and spend time with others and travel. The budget for entertainment spending creates a solution which enables people to maintain their social activities.

Emergency Fund Contribution

Retirees face unplanned expenses which include medical costs and home maintenance and family obligations. The practice of setting aside funds every month will create a financial buffer which prevents future economic pressures.

Insurance and Miscellaneous

The combination of home insurance and low-cost subscriptions and gifts and unplanned small expenses forms this category. This adaptable category enables organizations to handle their unpredictable financial commitments.

Savings or Family Support

It would not be wrong to say that some retirees continue saving or support children and grandchildren. The decision relies on their financial situation and their individual life goals.

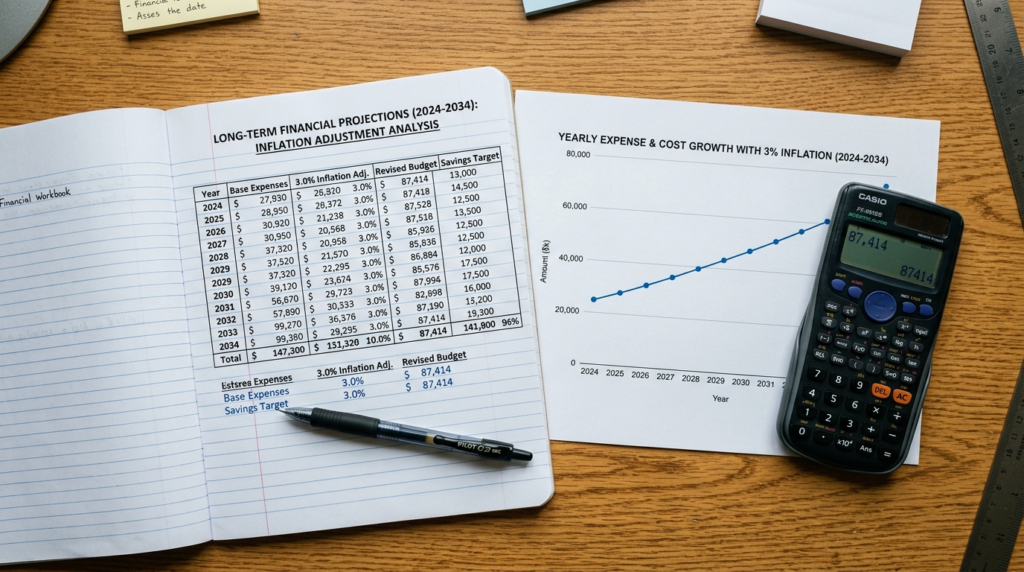

Inflation Adjustment Planning

Costs don’t stay the same. Retirees who want to maintain their spending power throughout their retirement years establish a budget which includes 3-5 percent yearly inflation increases for healthcare expenses an