Building a successful business means more than just generating more sales. Smart founders also make diligent efforts to see how much profit is left after taxes. Tax regulations differ among business types, industry, and location, but savvy business owners are adept at tax planning to maximize efficiency and contribute to long-term growth. Business owners can learn from common strategies that successful entrepreneurs employ to make better financial decisions and stay within the bounds of the tax laws that apply.

Choosing the Right Business Structure

The legal nature of a business may have a significant impact on taxation. As the company expands, many founders will regularly check if it’s best to continue operating as an LLC, S corporation, or corporation. A business that started as a sole trader can be more profitable and may require a different structure as the business grows.

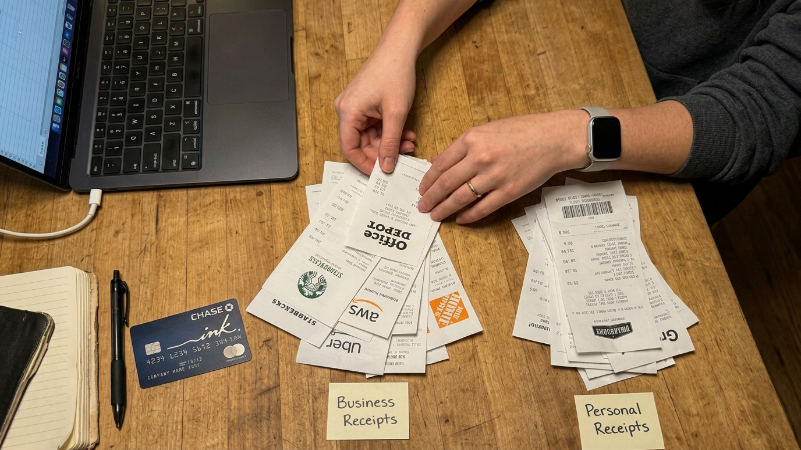

Separating Business and Personal Expenses

Entrepreneurs practice good business ethics by keeping personal and business finances separate. When tax preparation is simplified, it is easier to accurately identify legitimate business deductions, and organized records can make preparing taxes easier. Keeping business bank accounts and company credit cards can make bookkeeping and expense tracking easier.

Taking Advantage of Available Deductions

Many business owners lower their taxable income by taking advantage of tax deductions that are available for office expenses, software subscriptions, equipment, travel, professional services, and more. Qualifying technology tools, accounting services, and business-related education expenses are often deducted by startup founders.

Timing Income and Major Purchases Strategically

Some of the founders use professionals in the field of tax management to handle the timing of revenue recognition and huge business investments. This can sometimes be one way to help smooth out the year-over-year fluctuations in taxable income. Depending on business conditions, the timing of certain purchases or planned investments could impact tax results.

Using Retirement and Investment Accounts

Private business owners may make contributions to retirement plans that can offer tax benefits and contribute to long-term wealth building. These accounts can also enable founders to diversify outside of the business. Options such as SEP IRAs and Solo 401(k)s are commonly discussed among self-employed entrepreneurs and small-business owners.

Monitoring State and Local Tax Obligations

Tax requirements may vary as businesses expand into new markets. Tax planning is an issue that many founders overlook, and they end up with unanticipated tax obligations later on.

Working With Tax Professionals Early

Entrepreneurs, like many people, prefer to get professional tax advice before they have any issues rather than during tax season. It is often better to plan than to make changes at the last minute.

Reinvesting Profits Thoughtfully

It would not be wrong to say that some founders invest profits into growth activities like equipment, manpower, technology, or research and development that can also impact overall tax planning.