You don’t need to use a credit card regularly, but leaving it untouched for too long can quietly affect your finances. Your financial situation will be affected when you leave your credit card unused for an extended period. Credit card issuers track inactivity, and while there’s no universal cutoff, long gaps can trigger account reviews, limit reductions, or closures. Additionally, your credit score will experience an indirect effect from your inactive periods.

There’s No Official Deadline

Indeed, there’s no official deadline for inactivity but many issuers begin to examine your account after six months to a year without use. Also, your complete profile determines the outcome because credit cards with minimal usage, no annual fee, and low credit limits will undergo assessment more than premium, actively used accounts.

Why Banks Close Inactive Cards

Banks see no financial gain from inactive credit cards. Financial institutions use account closure as a method to decrease security threats while increasing their available credit resources. If your card remains unused for too long, the issuer may decide to close it.

How Closure Impacts Your Credit Score

Your total available credit will decrease when you close a credit card account, and your credit utilization ratio will increase when you have outstanding balances on multiple credit cards. The loss of available credit will decrease your credit profile strength even when you maintain a zero balance.

The Hidden Impact on Credit History Length

The value of older cards exists because they boost your account age average, which serves as an essential credit scoring component. Your account age will decrease when you close an old unused card because it removes an account that existed before your recent accounts.

Credit Limit Reductions Can Happen First

Before closing an account, some issuers reduce your credit limit. The effect on your utilization ratio remains less visible but still impacts your credit score. Therefore, in this case, your credit limit may suffer first with reduced points, even if you’re not actively using the card.

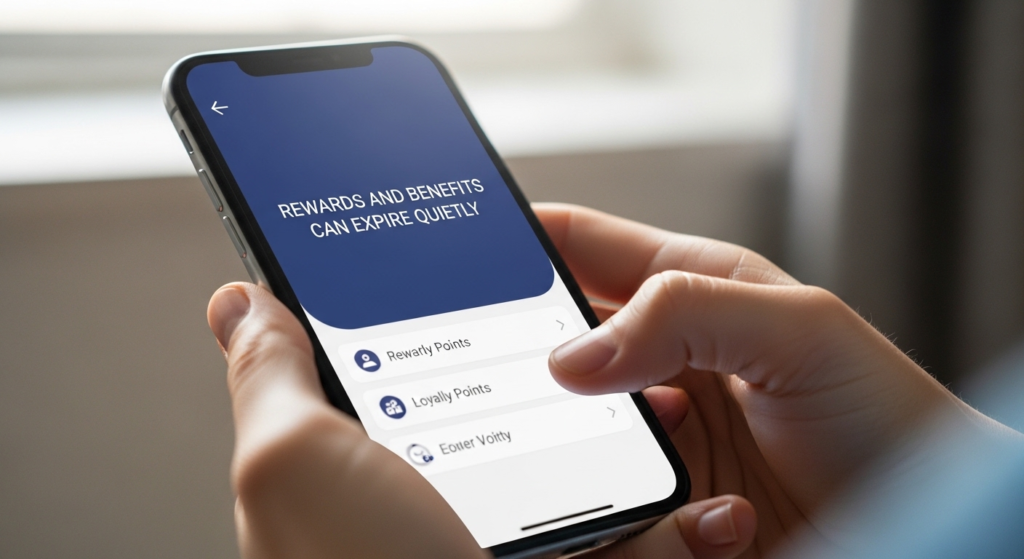

Rewards and Benefits Can Expire Quietly

Some cards require periodic activity to keep rewards valid. The points and cashback will vanish together with the travel benefits after the card remains inactive for an extended period. The information exists within the terms and conditions but remains hidden until after the customer has reached the point of no return.

How Often You Should Use It

A good rule of thumb is to use your card once every 2–3 months. The account remains active when users make any purchase. For example, making third-party subscriptions, paying for fuel, or grocery purchases. This helps credit cards be active and improve credit scores over time.

When It’s Okay to Let a Card Go Inactive

Not all cards need to be actively used forever. It may be okay to let a card go if you already have sufficient credit limits elsewhere or it has an annual fee you don’t justify. In such cases, closing it yourself gives you more control.