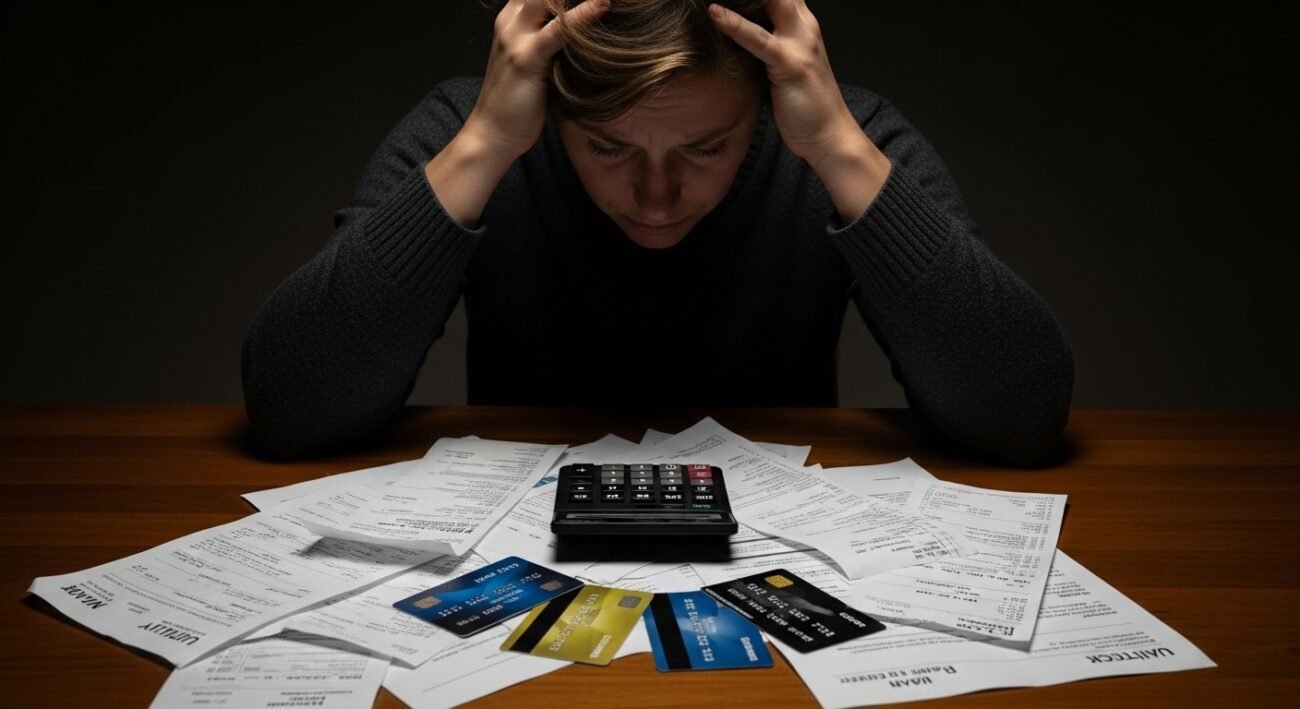

Debt may be helpful when it is utilized in a reasonable manner but some of these financial habits can easily turn into a trap. A large number of individuals are ending up in long-term debt without understanding how simple actions, such as making minimum payments or borrowing with a high-interest rate, can slowly accumulate to create an overwhelming debt. What may seem to be a temporary fix may turn out to be years of debt, tension, and economic stakes. The most important thing to do to prevent this trap is to know its formation process and be able to identify the red flags at an early stage. It is possible to secure your own financial future by making smarter decisions now and staying out of the loop that has already hit millions of households.

Living on Credit to Cover Daily Living Expenses

Credit cards can be used to purchase things on a daily basis and this may lead to dependency. Balance increases at a higher rate than they can be recovered when income is unable to pay regular expenditures.

Making the Minimum Necessary Payments

Minimum payments are only meant to keep the accounts active and not to wipe the debt. The interest continues to accrue, that is the cumulative repayment is significantly bigger with time.

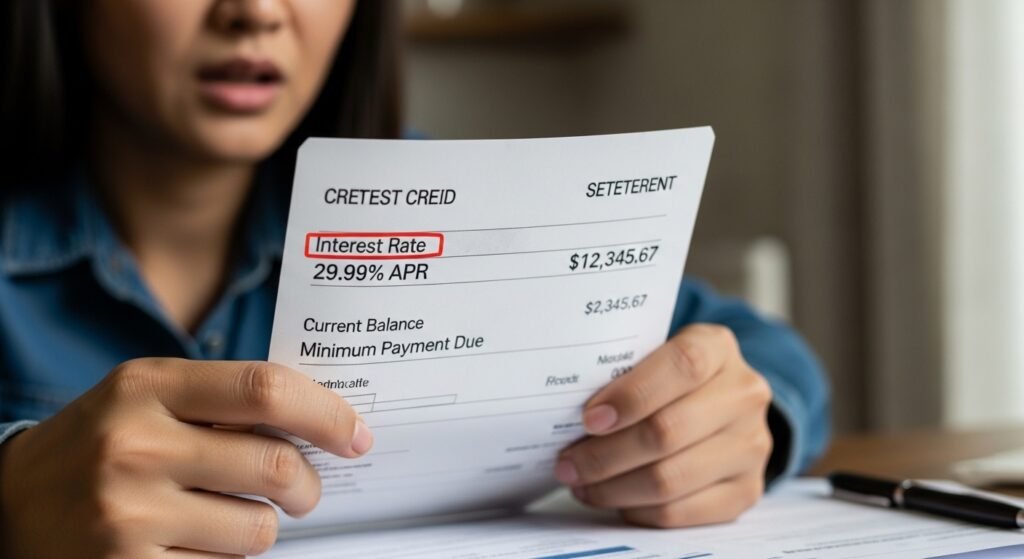

High-Interest Borrowing

With high-interest rates on loans and credit cards, the process of repayment becomes a lot more difficult. A simple balance can grow exponentially when there is interest made each month.

Neglecting Little Red Flags

The very first words of financial ill health include late payments, increasing balances, and frequent borrowing. Ignorance causes further debt issues.

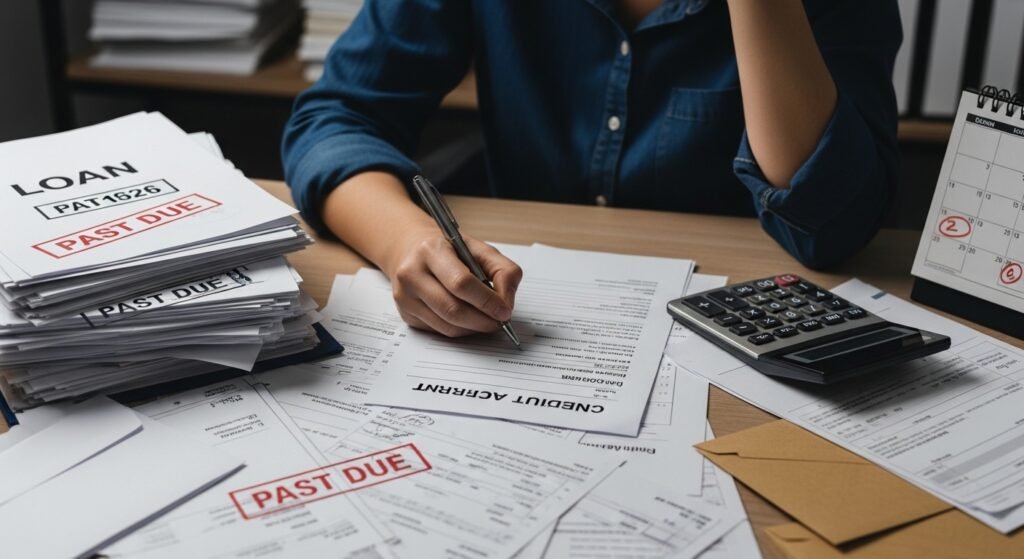

Using New Debt to Pay Old Debt

Borrowing money to settle the current debt is a vicious circle. Although this can be a relief in the short term, it can also tend to increase overall liabilities.

Lack of a Clear Budget

Income and expenses are not well understood and with this, it becomes easy to spend. A basic budget is used in order to manage expenditures and avoid credit dependency.

Emotional Spending

Unnecessary purchases may be caused by stress, boredom, or impulse buying. In the long run, emotional spending accumulates and leads to long term debt.

Failing to Develop an Emergency Fund

Unforeseen costs tend to state individuals into debts. The financial emergency can be minimized by having even a small emergency fund that will ensure you do not have to resort to credit during financial crises.

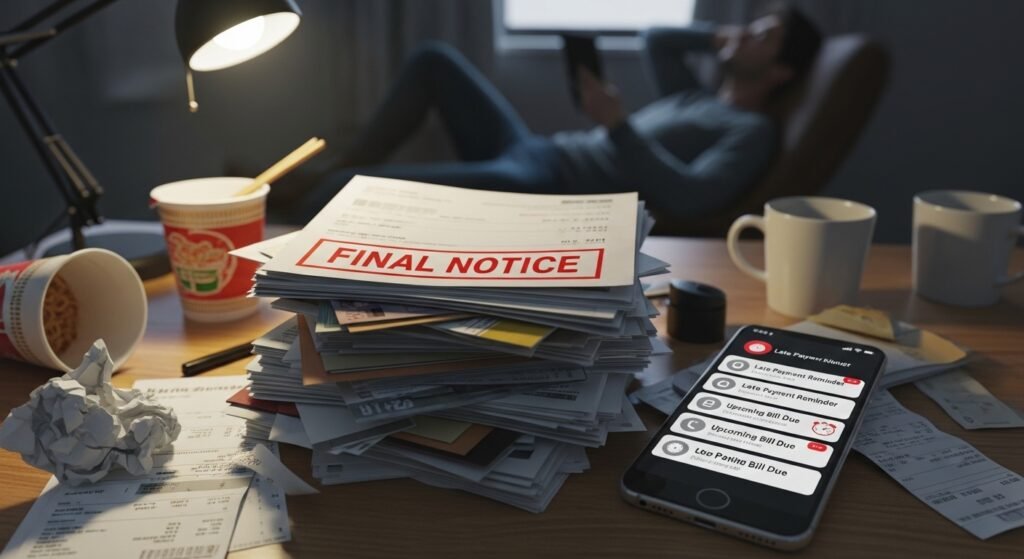

Missing Payment Deadlines

Penalties and increased interests, as a result of late payments. These charges eventually render debt even more difficult to eradicate.

The Way Out of the Trap

Destructive debt habits need a sense of discipline and awareness. Financial stability can be significantly enhanced by paying above the minimum wage, restricting usury lending, and having a strict budget.