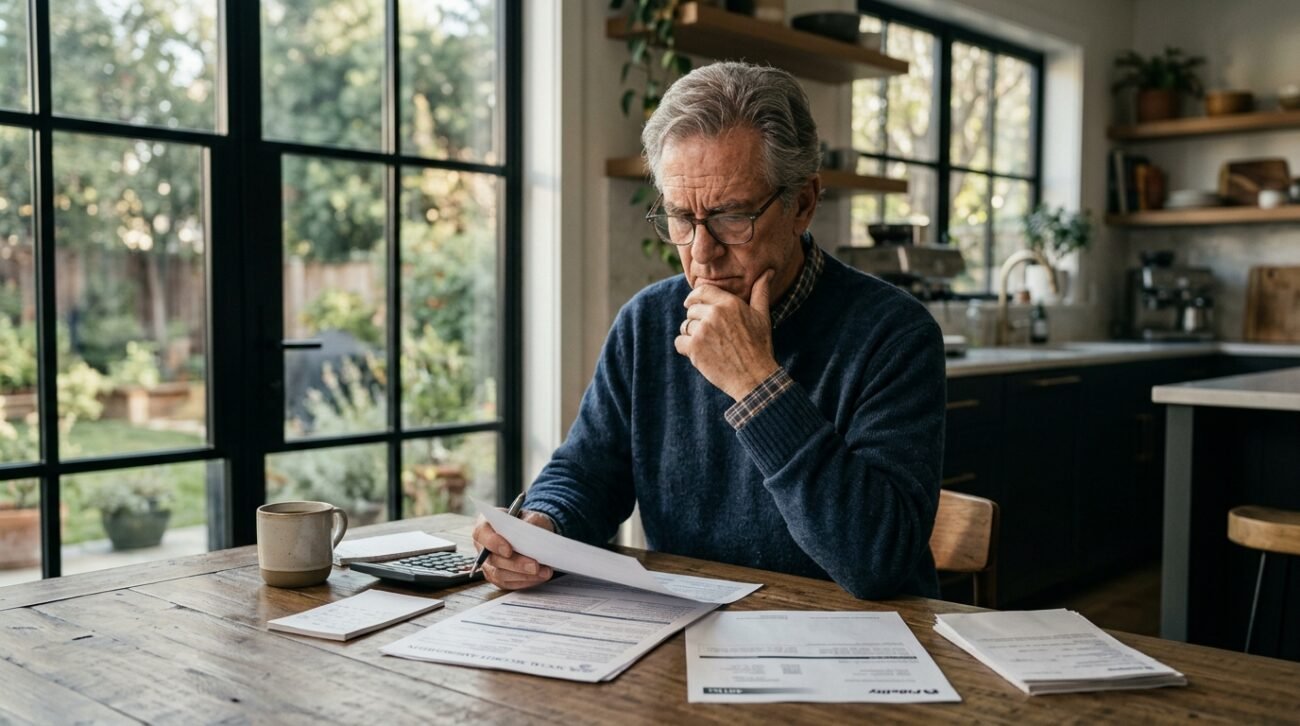

Many Americans feel that they will receive an ever-increasing benefit for their Social Security if they wait long enough to retire. The advantage of this method is that you can receive the biggest monthly check, but some retirees are taken aback to find their monthly payouts may actually be less over time. Other financial considerations, like taxes, Medicare costs, debt collections, and other things, can take a toll on budgets. It is more important than ever to know why this is so if you are a retired person who is looking to secure your finances in the future.

Social Security Benefits

Social Security benefits increase by a percentage each year up to age 70 for workers who delay retirement past full retirement age. According to the Social Security Administration, benefits accrue at a rate of two-thirds of 1% (0.66%) for every month you postpone claiming after reaching FRA.

Benefits Stop Growing After 70

Delayed retirement credits no longer accrue after age 70. That would mean that the retirees have already hit the maximum monthly benefit allowed by the current rules. There is no additional financial incentive to wait beyond this point, as benefits will not increase further.

Payments Often Decline After Age 70

An analysis of SSA data shows that monthly benefits are slightly reduced after the age of 70. The official formula does not necessarily reduce benefits, but many retirees end up with less income each year.

Taxes Can Quietly Reduce Monthly Checks

If retirees have other income from pensions, investments, or employment, up to 85% of Social Security benefits could become taxable, reducing the benefit amount they receive.

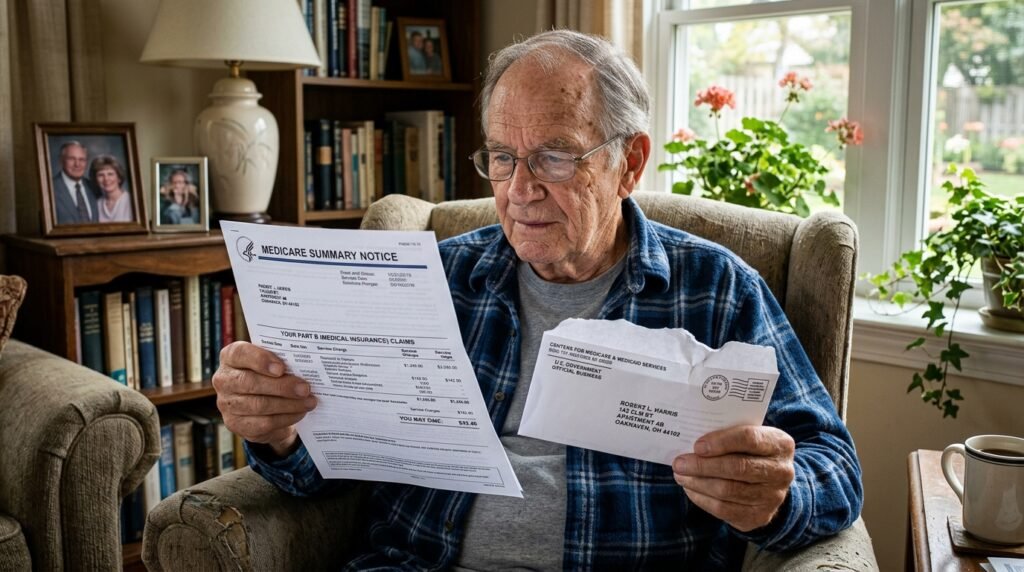

Medicare Premiums Keep Rising

Medicare Part B premiums will be deducted automatically from Social Security benefits. When health care expenses and income increase, these deductions can take a significant bite out of each paycheck.

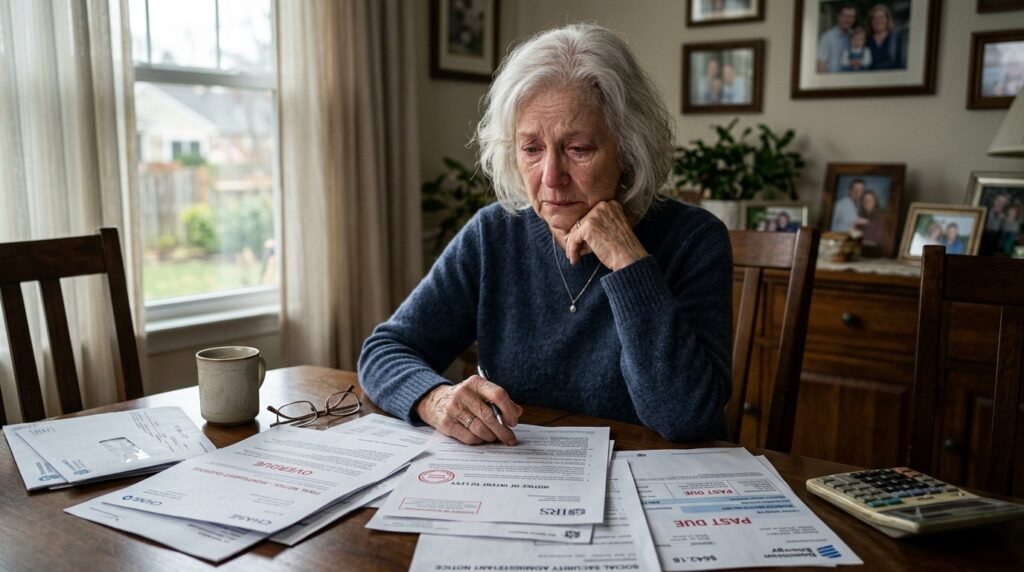

Debt Collections Can Also Impact Payments

The Treasury Offset Program allows the government to recover unpaid amounts of debt, like back taxes, student loans, or benefit overpayments, by withholding a portion of Social Security benefits.

Lifetime Earnings Strongly Affect Retirement Income

Benefits are computed based on a worker’s average of the highest 35 years of earnings, adjusted for inflation. Longer working lives, higher lifetime earnings, mean higher retirement benefits.

Maximizing Benefits Requires Long-Term Planning

Retirement age is not the only factor that determines retirement income, experts say. Retirees’ net monthly income is a major determinant of the amount of taxes, health care expenses, debt, and even financial planning.