Unexpected expenses, also known as unanticipated events, happen. It does not matter how well a household is planning; emergencies will develop, such as a hospitalization, unexpected home repair, job loss, or a family emergency, and the source of emergency cash becomes an issue very quickly. Money that a household has saved in its own funds should be used first; thus, all sources of emergency cash should be ranked from the least expensive with potential long-term financial problems to the most expensive with little or no potential for long-term financial problems. This ranking is intended to compare several common sources of emergency funds.

Emergency Funds and Short-Term Savings

Your own savings are the ideal source of cash for an emergency. Money in your account is kept in a checking account, a savings account, a money market account, or short-term investments like T-bills, and certificates of deposit (CDs) are immediately available to you.

Low-Risk Investments in Taxable Accounts

Another class of funds that can be used as an emergency fund is the money that you have invested in low-risk taxable investments, such as bond funds. If you can sell these in an emergency, you will get cash more quickly than if you had taken out a high-interest-rate loan, and you will avoid the negative consequences of borrowing.

Roth IRA Contributions

One of the unique features of Roth IRAs is that contributions to a Roth IRA can be withdrawn at any time for qualified distributions. However, withdrawing the principal of a Roth IRA will reduce the principal of the retirement savings, and therefore will reduce the amount of funds available for growth.

Life Insurance Cash Value

While accumulating a cash value in a whole life insurance policy or a universal life insurance policy can be a long and difficult process, the good news is that if you have built up a cash value in your policy then you may be able to access the funds that you have put into your policy in the past in an emergency.

401(k) Loans

A 401(k) loan allows workers to borrow from their retirement accounts while paying interest back into their own savings. Interest rates are often lower than many consumer loans, but borrowing reduces retirement growth potential and creates risks if employment ends unexpectedly.

Home Equity Lines of Credit

Homeowners may be able to borrow against accumulated home equity at relatively favorable interest rates. While HELOCs can be useful in emergencies, they put a valuable asset, the home itself, at risk if repayment becomes difficult.

Hardship Withdrawals From Retirement Accounts

Unlike loans, hardship withdrawals permanently remove money from retirement accounts. These withdrawals are often subject to income taxes and may trigger additional penalties for younger account holders, significantly reducing the amount ultimately received.

Reverse Mortgages

For homeowners who are 62 and older, reverse mortgages can unlock home equity without needing to pay it back right away. But the fees, interest costs, and that general loan complexity can make it a costly path, and it also tends to lower future home value for heirs, in a sort of indirect way.

Margin Loans

Investors can sometimes borrow against securities held in brokerage accounts. While this may help avoid selling investments during a market downturn, margin loans carry significant risks because falling asset values can trigger forced sales or additional cash requirements.

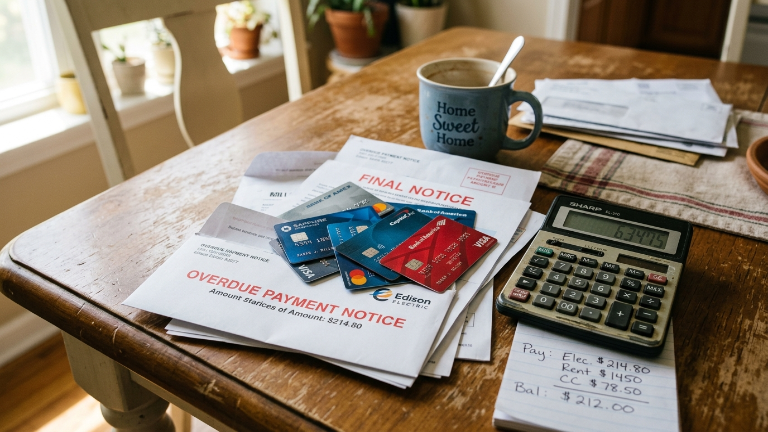

Credit Cards

Credit cards are often seen as the least desirable kind of emergency cash, simply because the interest rates are high, and you can end up in a long, drawn-out debt spiral. Minimum payments usually do not lower your balance much, so it becomes pretty easy for short-term money trouble to turn into a much bigger financial problem over time.