When Americans turn 62, they start to qualify for Social Security benefits, and many are eager to receive the money as early as possible. However, premature filing will permanently decrease the monthly benefit. Before finalizing your claim, it’s crucial to consider your financial circumstances and ensure that your retirement income plan aligns with your future objectives.

You Can Start Benefits at Age 62

The Social Security benefit can give retirement benefits as early as age 62. Even though this might sound attractive, the earlier one turns 65, the lower the monthly payments will be compared to being at full retirement age or older.

Filing Age Affects Your Monthly Benefit

When you file for Social Security has a huge impact on the amount of money you receive per month. Generally, the longer you wait, the higher your payment will be, and the sooner you claim, the less you’ll get.

Benefits Stop Growing After Age 70

There’s no point waiting past 70 to receive Social Security benefits, although delaying the process does boost the benefit amount. That’s when any retirement benefits you accrue for the year will cease, and that’s the most recent date that most experts suggest for filing.

Calculate Your Retirement Income Needs

Before seeking benefits, try calculating how much of an annual income you’ll require in retirement. Consider both needs, like housing or health care, and wants such as travel, entertainment, and hobbies.

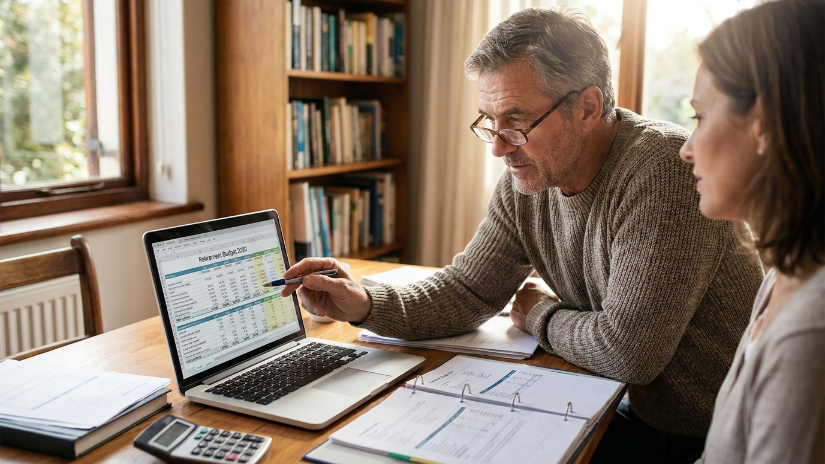

Review Your Other Income Sources

Social Security might not be the only source of retirement income. When determining if you can afford to retire, think about taking money from retirement accounts, pension plans, investments, rental properties or part-time jobs.

Compare Income Needs

After you have an idea of your expenses and the other sources of income, calculate how much income your Social Security benefit will have to make up for. This comparison can help you to determine whether you will receive sufficient income if you file for your insurance benefits now or wait.

Even Small Shortfalls Can Matter

It may not look like much of a difference in the first few hundred dollars per month. But that can turn into a problem over a long retirement, which may be decades long, and can be stressful on your finances and your budget.

Unexpected Expenses Are Inevitable

During retirement, other unexpected expenses such as healthcare costs, home repairs, and inflation can come up. The delay in claiming benefits might result in a bigger payout and extra financial cushion if unanticipated costs arise.

Eligibility and Readiness

Being eligible and ready are not the same thing. Although many people can start collecting benefits at age 62, there could be a huge difference in their long-term financial situations if they wait to collect benefits and maximize their payments.

Improve Retirement Security

Social Security is among the only retirement income sources assured for life. Analyzing your finances, income needs, and long-term objectives can help ensure that your benefits provide a comfortable retirement.