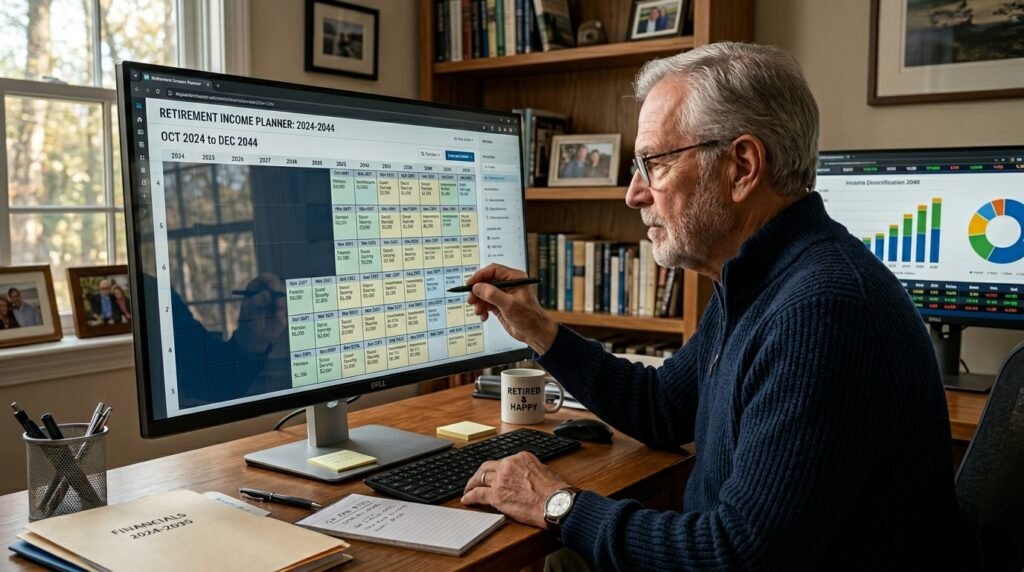

When retirement savings goals are linked to actual spending patterns, it can be easier to plan for retirement. As one of the ideas that has come up in the news recently, the “Rule of 240 Paychecks” concept is looking at retirement savings over a very long period of time by replacing one month’s paychecks. Rather than simply thinking in terms of all up-front savings, it is the number of future monthly income checks that retirement may require that are considered. It is important to grasp this point to set a realistic and consistent retirement plan.

Focuses on 20 Years of Retirement Income

The term “240 paychecks” is derived from the notion that someone retiring for 20 years means they’re receiving a paycheck approximately 240 times a year. This model can be used by financial planners to help individuals understand how long their retirement savings might need to last.

Retirement Length Continues Increasing

Many Americans nearing age 65 today could live 20 years or more in retirement because of current life expectancy growth, the Social Security Administration reports.

Monthly Spending Often Matters More

Many times, financial advisors will tell you that the sustainability of monthly withdrawals is the key to retirement success, and that number isn’t that important.

Average Retirement Spending Remains Significant

Recent consumer expenditure surveys by the Bureau of Labor Statistics showed that the median spending by an adult household (age 65 and older) was more than $57,000 per year.

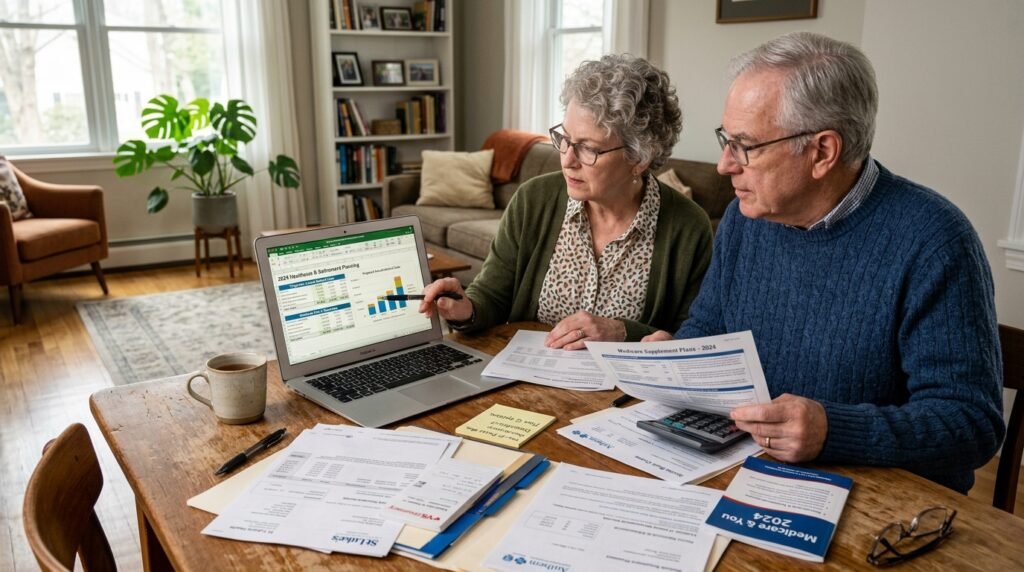

Continue Affecting Retirement Budgets

According to Fidelity Investments, the average retired couple may require approximately $315,000 for healthcare-related expenses during retirement. Therefore, healthcare costs continue to affect retirement budgets.

Covers Only Part of Retirement Income

The benefit received from Social Security can be used to fund only part of the retirement income for many individuals. Money earned from 401(k), pensions, IRAs, and savings is still significant to pay the bills each month.

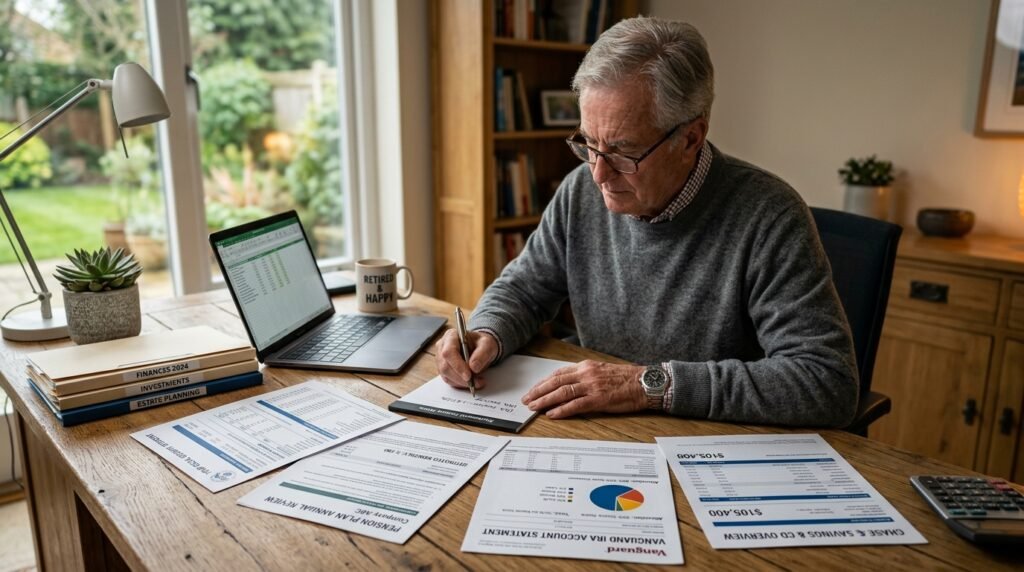

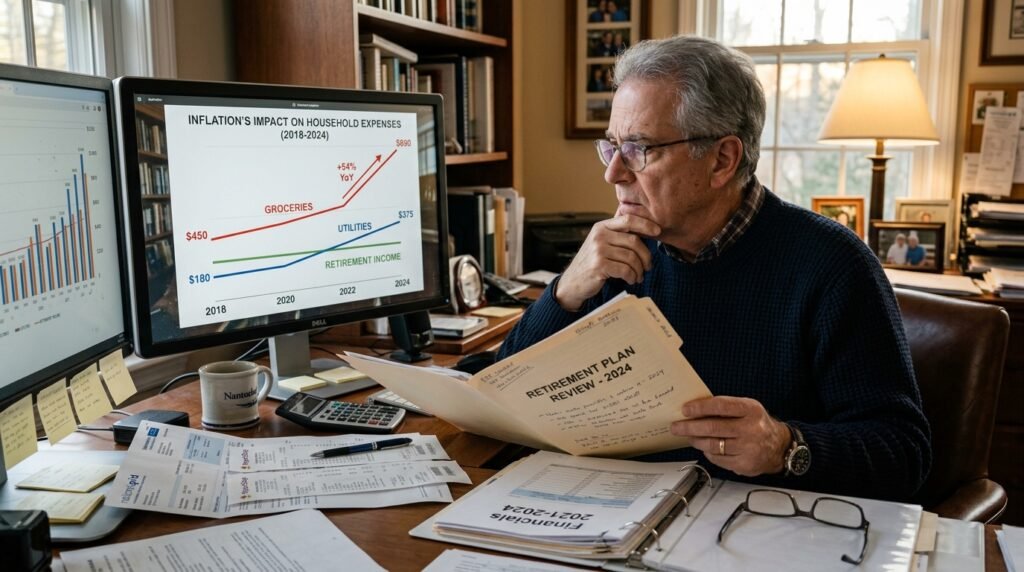

Reduce Purchasing Power Over Time

Inflation over 20 years can make a big difference to retirement budgets. Withdrawals may need to begin to increase later in retirement years for housing, health care, food, and utilities.

Encourage Flexible Withdrawal Strategies

Many advisers don’t suggest that you make a set withdrawal amount for years, but suggest that retirement spending vary in the future depending on investment performance, inflation, and lifestyle requirements.

Habits Usually Matter Most

It’s important to note that some retirement experts say that regular, consistent contributions and disciplined saving can be the greatest factor in retirement readiness than simply trying to accurately predict future market performance.