One of the largest financial decisions retirees will make is when to start taking their Social Security benefits. Benefits may start as early as age 62, but may also provide a higher lifetime income the longer they’re delayed. Knowing the age impact on payments may have a significant long-term difference on retirement security.

You Can Claim Benefits Between 62 and 70

Social Security benefits may be started as early as 62 or as late as 70 years of age. You can wait past 70, but there isn’t an extra discount for waiting beyond that age.

Claiming Early Lowers Payments

If taken before full retirement age, Social Security benefits permanently decrease. If you file when you’re young, those payments may be as low as 70% of your regular benefit amount.

Delaying Benefits Can Increase Income

Delayed retirement credits are awarded to retirees who delay their retirement. Those credits can increase monthly payments by up to 24%, which means larger guaranteed income payments during retirement.

Early Filers Receive More Checks Over Time

Those who pull the trigger on benefits will be paid for a longer duration. Each monthly payment is less, though, which can impact long-term financial security if retirement is many decades long.

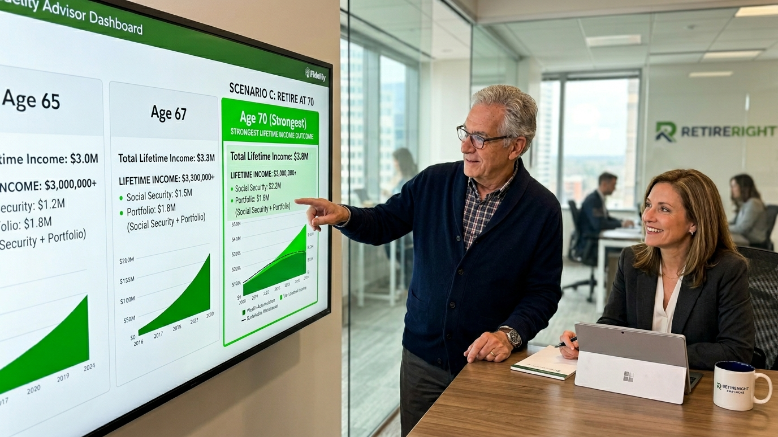

Waiting Often Produces Greater Lifetime Wealth

Many studies have shown that many retirees can end up with greater total wealth over their lifetimes by deferring Social Security benefits. Longer life expectancies mean larger monthly checks often outweigh the value of claiming earlier.

Strongly Favored Waiting Until 70

The 2019 United Income study found that 57% of retired Americans had the most lifetime wealth by waiting to collect Social Security until age 70, and few earned the most by filing before age 64.

May Boost Retirement Spending

The National Bureau of Economic Research’s research showed that for many workers, delaying benefits till age 70 raised their potential lifetime earnings by a substantial margin and significantly boosted the median household wealth.

Retirement Savings Play a Major Role

For those who can save or generate investment income to support their retirement, waiting until 70 is a better option. A solid retirement plan can help support a person’s living costs in the years leading up to retirement, as well as Social Security benefits.

May Improve Financial Security

A large proportion of those who fail to claim benefits end up staying in the job longer than they need to. More years of working means more years of income, more years of retirement savings, and more years of Social Security payments.

The Best Claiming Strategy

While data often favors delaying benefits, the right choice still depends on personal health, retirement savings, employment plans, and income needs. With careful consideration of your finances, you can make the most of your long-term retirement security.