Social Security benefits can be quite different among retirees. Some Americans are collecting over $5,000 a month, while others are collecting closer to $1,200 a month. There are typically three main factors that distinguish the difference: income history, years of service, and age of retirement.

Benefits Aren’t Equal for Everyone

The Social Security system is intended to replace various levels of salaries or income in accordance with the worker’s earnings history and retirement options. Dramatically different monthly payments can be paid to two retirees who have paid into the same program during their careers.

Earnings Matter Most

Benefits primarily depend on the top 35 years of an employee’s inflation-adjusted wages. The person’s amount will be much smaller if he or she worked for 20 years at a modest income, as opposed to a worker who worked for 20 years and earned close to the maximum taxable income.

Higher Earners Build Larger Benefits

Average indexed monthly earnings are substantially higher when workers have high salaries throughout their careers. This means that the amount they can expect to receive each month in retirement is much higher when they receive SS benefits.

The Formula Uses Bend Points

The formula that Social Security uses employs a range of income called “bend points. The percentage replacement of earnings is greater for lower-income earners, but the dollars are much greater for higher-income earners.

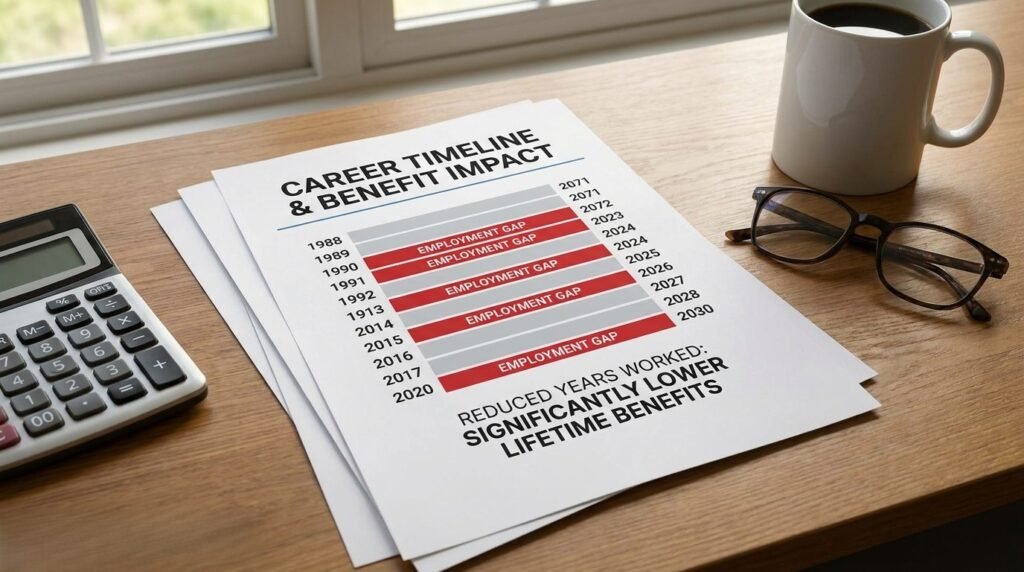

35 Years Can Hurt Benefits

Benefits are calculated based on a full 35-year work record. If one person works just 25 years, the other 10 years are dropped as zeros, which decreases the total earnings, and the monthly payments will be significantly lower.

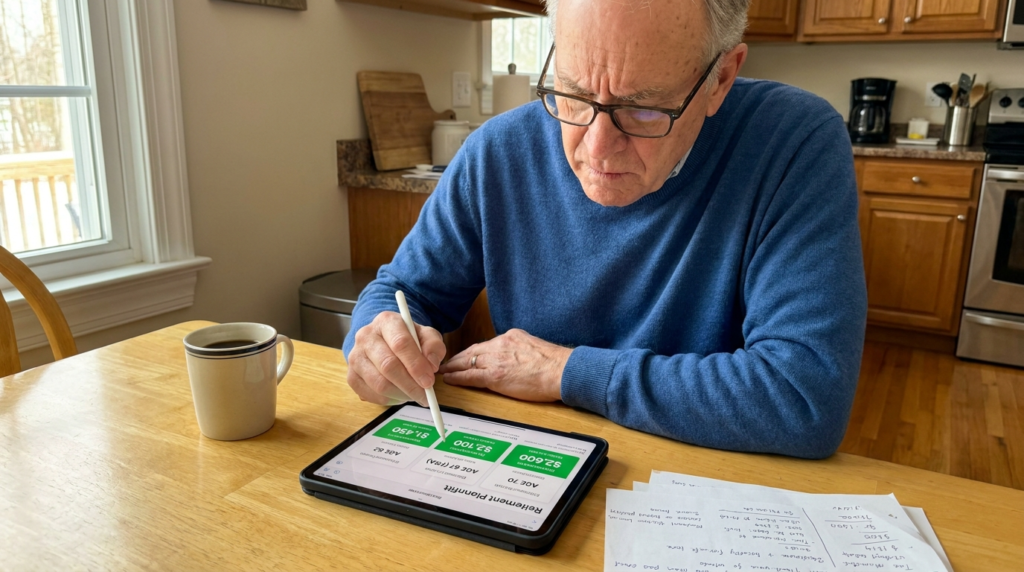

Claiming Age Has a Massive Impact

One of the most important things impacting benefits is when retirees begin to receive their Social Security benefits. Benefits are also reduced permanently because they are filed before full retirement age, and benefits are paid at a much higher rate if they are not filed until after the full retirement age.

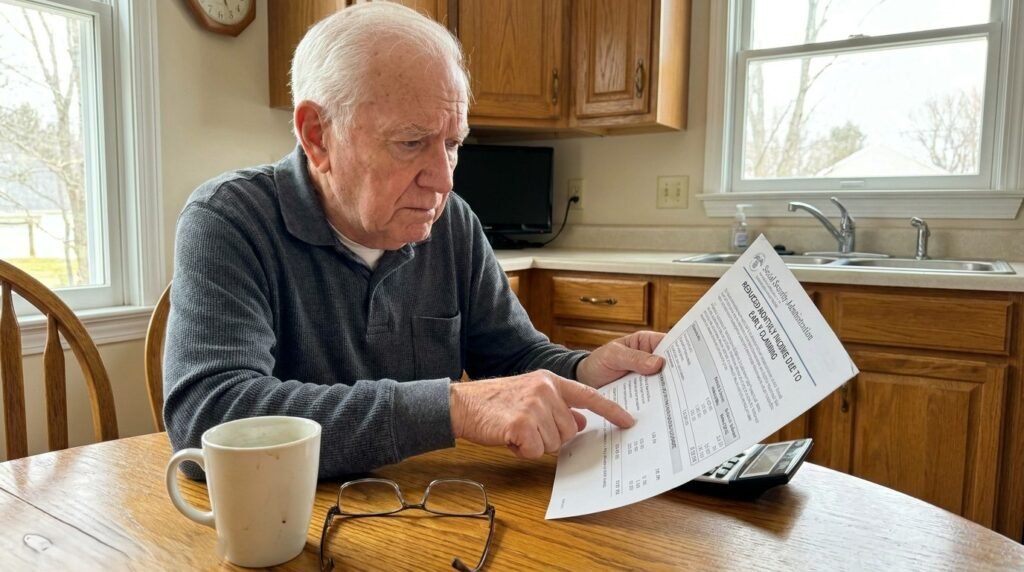

Claiming at 62 Can Reduce Payments

For any worker born in or after 1960, full retirement age is 67. One can lose about 30% for each month they claim benefits at age 62, resulting in a smaller amount of benefits that will continue to be received throughout retirement.

Waiting Until 70 Increases Monthly Income

Delayed retirement credits are earned at approximately 8% per year until age 70. This increase may mean hundreds of dollars in additional monthly income over time, and larger increases to the cost-of-living for future years.

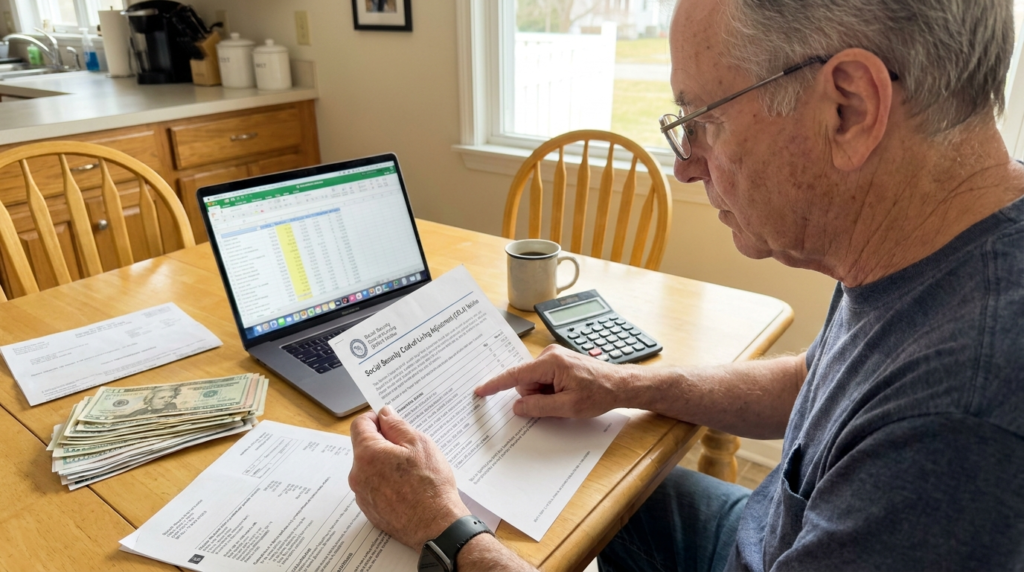

Inflation Makes Larger Benefits

The cost-of-living adjustments are based on the monthly payment amount of a retiree, and they are applied once a year. The larger the benefit, the greater the dollar gains in the future, and the better retirees will be able to afford their growing healthcare, housing, and cost-of-living expenses.

Claiming Early Can Be Difficult to Reverse

One of retirement’s most difficult mistakes to correct is claiming too early, according to financial experts. In good health and with savings or other income available, waiting a few years more might be very advantageous for retirees.